Introduction

Microfinance has helped many Africans access money when traditional banks were not an option. Today, the role of technology in African microfinance is more important than ever. With the rise of digital tools and better internet access, it is now easier, faster, and cheaper for people to get loans, save money, or even buy insurance.

Technology is opening the door to more opportunities. More people, especially in hard-to-reach areas, can now enjoy financial services. This is changing lives and helping small businesses grow across the continent.

Overview of Microfinance in Africa

In Africa, microfinance institutions (MFIs) give small loans to people who need money to start or grow businesses, pay school fees, or cover emergencies.

These services are helpful. However, they can also be expensive and hard to manage, especially in rural areas where banks are far away. Many MFIs struggle with high costs and slow services.

This is where technology comes in. Mobile phones, digital payments, and online platforms make it easier for people in faraway places to get the help they need. Now, someone in a small village can borrow money or save without needing to visit a bank.

Importance of Technology in Expanding Financial Access

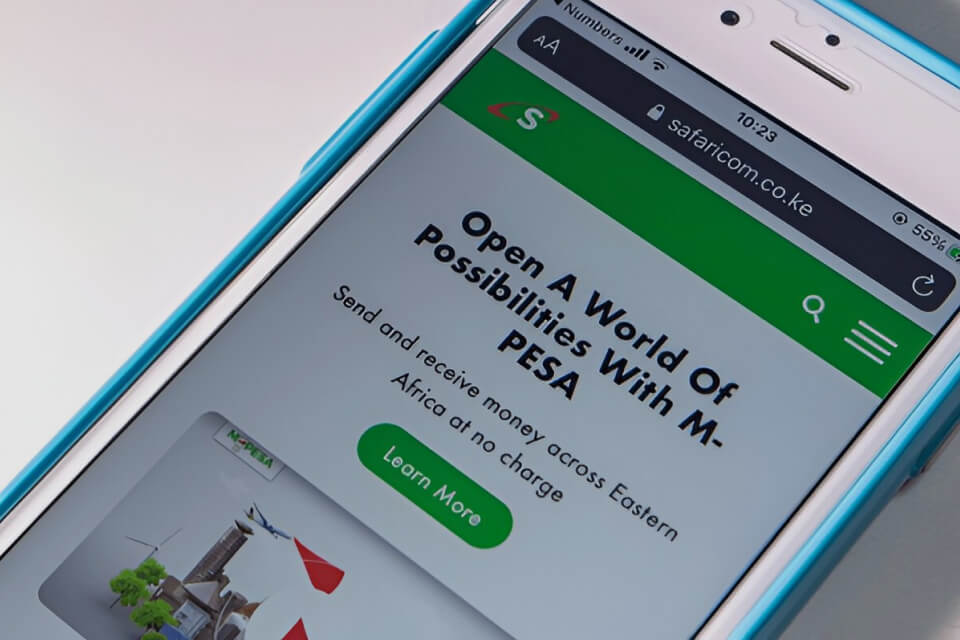

Technology makes everything easier and faster. For example, mobile money apps like M-Pesa in Kenya have changed how people handle money. With just a phone, users can send money, save, or borrow.

Also, new tools are helping lenders decide who is safe to lend to. They use things like mobile usage and payment history instead of just paperwork. This makes it easier for people who don’t have bank accounts or official records to get help.

Even better, smart tools like artificial intelligence and secure systems like blockchain are making sure that lending is safer and fair for everyone. These tools are especially helpful for women, youth, and small business owners who are often left out.

Setting the Stage for Digital Transformation in Microfinance

Things are changing fast. As more people get internet access, more MFIs are using digital tools to improve their services.

One exciting change is “embedded finance.” This means banking services are included in other apps, like farming or shopping platforms. So users don’t need a separate app to borrow or save. It’s all in one place.

These changes also support the impact of microfinance on African social enterprises. As small businesses and community projects grow, they create more jobs and support local economies. This is a clear example of the growing role of technology in economic development.

Technological Innovations in Microfinance

One of the roles of technology in African microfinance is to help microfinance institutions, or MFIs, reach more people and provide loans more quickly, safely, and easily. This is great for small businesses and social enterprises across Africa. With technology, financial services are becoming more fair and available to everyone. Now, let’s explore some of the tools changing how microfinance works on the continent.

Digital Loan Application and Approval Systems

First, let’s talk about how people apply for loans. In the past, they had to visit a bank or MFI branch. This took time, energy, and money. But now, thanks to digital loan systems, many people can apply using their phones or computers.

This change is important. For example, in some countries, MFIs allow users to request and track loans online from anywhere. This is especially helpful for people in rural areas where banks are far away. Because of this, more people can access financial support. These tools also help MFIs approve loans faster and avoid mistakes that usually come with paper forms. So, microfinance for African small businesses is becoming much easier and more accessible.

Use of Artificial Intelligence for Credit Scoring

Next, artificial intelligence, or AI, is helping MFIs decide who can get a loan. Usually, banks look at your credit history. But many people in Africa don’t have this kind of record.

Now, with AI, MFIs can study other information. For example, they can look at how often someone uses their phone, pays their bills, or even how they act online. This helps lenders understand if a person is likely to repay a loan.

Even better, AI can spot early signs that someone might struggle with repayment. This allows MFIs to step in and help before it’s too late. Because of this, loans are now more fair and better managed. It also means more people are included in the financial system, which supports the impact of microfinance on African social enterprises.

Cloud-based Data Management for MFIs

Another big change is how MFIs keep their data. Before, they used paper or local computer files, which could get lost or damaged. Now, many use cloud technology, which stores data safely online.

This makes it easy for staff to access important information anytime and from anywhere. For example, they can check loan details, payment history, or customer records quickly. As a result, operations run more smoothly. MFIs can also grow faster because they don’t need lots of offices or workers to keep up.

So, cloud systems are not only safe but also smart. They help MFIs serve more clients while saving time and money.

Integration of Blockchain for Secure Transactions

Finally, blockchain is starting to make a difference. Although still new, it is being used to make digital transactions safer and more honest.

Blockchain records each transaction in a way that cannot be changed. This helps prevent fraud and builds trust between lenders and borrowers. For people borrowing or saving money digitally, feeling safe is very important.

Even more, blockchain makes cross-border payments cheaper and faster. This can help African small businesses grow beyond their countries. And it gives them access to even more markets and customers.

Impact of Mobile Banking and Digital Platforms

Technology in African microfinance is changing lives. From small towns to big cities, mobile phones and digital platforms are helping people get the financial support they need. These tools are opening doors that were once closed, especially for people living in rural or underserved areas.

Expansion of Financial Services to Rural and Underserved Areas

In the past, many people in villages had no banks nearby. But now, thanks to mobile phones, they can save money, borrow funds, and even open accounts from their homes. This is a big deal. It means more people can grow small businesses, take care of their families, and improve their future.

More importantly, it allows African social enterprises to get funding faster and easier. These social-focused businesses can now do more good, all because digital tools are bringing banking services closer to everyone. The impact of microfinance on African social enterprises is stronger than ever before.

Reduction in Transaction Costs and Operational Overhead

Before mobile banking, banks had to build branches, hire many staff, and spend a lot on paperwork. That made things slow and expensive. But with digital tools, all of that has changed.

Now, sending money or repaying a loan can be done with just a few clicks or a short code on a mobile phone. This means banks spend less, and people pay less in interest. It also helps these services last longer and reach more people. For those offering microfinance for African small businesses, this is a smart and cost-saving way to operate.

Increased Customer Convenience and Financial Literacy

One of the best things about mobile platforms is that they are easy to use. Anyone with a phone can check their balance, send money, or repay a loan at any time. This kind of convenience encourages more people to save and stay on top of their finances.

Also, many of these apps teach users how to handle money better. They explain things like how to budget or understand loan terms. This builds financial literacy, which helps people make smarter decisions and avoid debt traps. When people know more, they can do more, and that means better lives and stronger communities.

Real-time Access to Savings, Loans, and Repayments

Today, everything moves fast, and banking is no different. With digital platforms, people can see their savings, get loan updates, and make repayments instantly. There’s no need to wait in long lines or fill out many forms.

This quick access builds trust between the people and the microfinance providers. It also helps banks understand their customers better by tracking how they use their phones and money. That makes it easier to give loans to small businesses that were once ignored. It’s another way the role of technology in economic development is showing up across Africa.

Case Studies of Technology-Driven Microfinance Solutions

Today, many Africans can access financial services even if they do not have a bank account. Thanks to mobile phones and digital tools, it is now easier, safer, and faster for people to send money, take loans, and grow small businesses. Let’s look at some real examples of how this works.

M-Pesa and its Influence on Micro-Lending in Kenya

One of the best-known examples is M-Pesa, a mobile money service that started in Kenya in 2007. Before M-Pesa, many people in rural and urban areas had no safe way to save or send money. But M-Pesa allowed users to send and receive money just by using a basic mobile phone.

Today, millions of Kenyans use M-Pesa. It helps farmers, small shop owners, and even market traders get paid without needing to carry cash. That means fewer risks and faster business. Even more exciting, people can now receive small loans directly through their phones. This has helped many women and families handle emergencies and grow small businesses. As a result, M-Pesa has had a huge impact on microfinance for African small businesses.

Tala and Digital Credit Scoring in East Africa

Another great example is Tala, a company that operates in Kenya and Tanzania. Tala gives loans to people who do not have a bank account or credit history. But how do they decide who gets a loan?

They use information from your phone, like how often you call or how you manage your texts and apps. This helps Tala understand if someone is likely to repay a loan. This is called digital credit scoring, and it allows Tala to make fast decisions without long forms or waiting.

Because of Tala, more people now have a chance to borrow money for school fees, small shops, or farming tools. This shows how the role of technology in African microfinance is helping more people build better lives, even without formal banking.

Partnership Models between Telcos and MFIs

In many African countries, telecommunication companies, also known as telcos, are teaming up with microfinance institutions (MFIs). These partnerships work really well. The telcos already have the technology and mobile networks. MFIs know how to manage loans and savings. Together, they can serve more people.

For example, in Kenya, the company behind M-Pesa works closely with banks and MFIs to offer easy loans through mobile phones. People can borrow small amounts without visiting a bank or filling out long forms. This teamwork makes it easier for people to access money and improve their businesses or homes. It also shows the role of technology in economic development, especially when both tech and finance work hand in hand.

Regional Examples of Successful Fintech-Microfinance Integration

It’s not just Kenya that is leading the way. Many other African countries are joining in. In Nigeria, companies like Renmoney let people borrow money or save through apps. No paperwork is needed, and the process is quick.

In East Africa, mobile apps connect loans and savings directly to your mobile wallet. This means you can borrow money and even pay for insurance using your phone. These services help more people manage their money, start businesses, and plan for the future.

Clearly, the impact of microfinance on African social enterprises is growing across the continent. Digital tools are breaking barriers and reaching people who used to be left out.

Challenges and Opportunities with Technology

Technology is changing how microfinance institutions work. It is making financial services easier to reach for people who don’t use traditional banks. This includes farmers, market women, and small business owners. But even with all the benefits, there are still some real challenges. Let’s explore the main issues and how they can be turned into great opportunities.

Digital Literacy and Access to Smartphones

First, one of the biggest problems is that many people don’t know how to use digital tools. This is called digital literacy. In rural areas or low-income communities, people may not know how to use smartphones or financial apps. Some only use phones to make calls or send text messages. Also, not everyone owns a smartphone that can run digital banking apps.

That is why it is important to teach people how to use these tools. When users understand how to manage money online, they can access more services and improve their lives. The good news is that more people in Africa are getting smartphones. This means more people can now use mobile money and microfinance services. As a result, access to finance grows and helps small businesses do better.

Cybersecurity and Fraud Prevention

Now, let’s talk about security. As more people use digital financial tools, the risk of cyber fraud also increases. Many users are new to online banking. This makes them easy targets for scammers. In the same way, microfinance institutions can face hacking or data theft.

To stop this, providers must invest in secure systems. It is also important to teach users how to stay safe online. For example, they should never share their PIN or click suspicious links. When users feel safe, they trust the system more. This trust will boost the use of microfinance for African small businesses and help grow the digital economy.

High Initial Cost of Tech Infrastructure

Another challenge is money. Setting up technology for microfinance is expensive. It costs a lot to buy good computers, software, and secure servers. Also, many rural areas still don’t have good internet or mobile network coverage. This makes it hard to offer digital services in those places.

But here’s the opportunity. Local companies and microfinance providers can team up. They can use cloud services and low-cost digital tools. This brings down the price and makes it easier for everyone to start. Over time, shared infrastructure will lower the cost and make services more available. This directly supports the role of technology in economic development by improving access to finance.

Opportunities for Local Tech Startups in Microfinance

Technology is opening doors for local startups. Across Africa, young innovators are building new financial tools. Some of these include mobile lending apps, agent banking systems, and digital platforms for saving or sending money.

These tools are designed to meet the real needs of people in Africa. They make it easy for microfinance institutions to serve more people, especially those in hard-to-reach places. As more startups get support from investors and governments, they can scale faster. This helps more people access affordable financial help. The impact of microfinance on African social enterprises and communities becomes even stronger.

Future Directions for Technology in Microfinance

Technology in African microfinance is making it easier, faster, and smarter for people and small businesses to get the financial help they need. As we look ahead, there are some big and exciting changes coming. These changes will help more people, especially those in underserved communities, grow their businesses and improve their lives.

Use of Big Data and Analytics to Improve Services

To begin with, one of the biggest changes in microfinance is how banks and lenders use information. Today, they collect data from many places, like mobile money apps and even social media. Then, they study this data to understand what people need and how likely they are to repay loans.

As a result, microfinance institutions can now make better decisions. They can offer loans faster and with less risk. Even small business owners who traditional banks used to ignore can now get help. This is a huge step forward. It shows the impact of microfinance on African social enterprises because more people can now access money to start or grow their businesses.

Growth of Decentralized Finance (DeFi) in Lending

Next, another exciting development is Decentralized Finance, also known as DeFi. This is a new way to lend and borrow money using blockchain technology. It does not need banks or middlemen. Instead, it connects people directly.

In many parts of Africa, DeFi is helping people access loans more easily. With peer-to-peer lending, borrowers can get money quickly and with fewer extra costs. This makes borrowing simpler and more open. Clearly, this trend supports the role of technology in economic development, by offering more options to people who were left out before.

Policy and Regulatory Support for Digital Microfinance

Still, technology alone is not enough. Good rules and strong policies are also important. Thankfully, many African governments are now stepping in. They are writing laws that support digital microfinance while keeping users safe.

For example, some rules now cover mobile money, online loans, and how customer data is used. These rules help build trust between lenders and users. They also protect people from scams or unfair treatment. In turn, this makes more people feel safe using digital finance. This kind of support is a major boost to microfinance for African small businesses.

Inclusive Tech Design for Gender and Youth Empowerment

Finally, we must talk about inclusion. In many places, women and young people still face more problems when trying to get loans. But the good news is that more tech companies are now designing tools just for them.

They are making apps that are easy to use, even on basic phones. They are also offering loans with flexible terms and in local languages. These small changes make a big difference. Now, more people can take part in the financial system. This pushes microfinance to truly reach those who need it most and brings hope to entire communities.

Frequently Asked Questions (FAQs)

1. What is the role of technology in African microfinance?

Technology helps microfinance institutions reach more people, process loans faster, and reduce costs by using mobile banking and digital platforms.

2. Can technology reduce transaction costs for microfinance?

Yes, digital tools cut down on travel and paperwork costs, making loan disbursement and repayments more efficient.

3. What are the main challenges with using technology in microfinance?

Challenges include high technology costs, limited digital literacy among staff and clients, and infrastructure issues like poor internet coverage.

4. What future trends are expected for technology in microfinance?

More use of AI, blockchain, and expanding mobile access will improve transparency, reduce fraud, and increase efficiency.

5. How does microfinance impact African social enterprises?

Microfinance, supported by technology, provides funding that enables social enterprises to grow and create positive economic changes in communities.

Conclusion

The role of technology in African microfinance is transforming how financial services reach millions of people. By using mobile banking and digital platforms, microfinance institutions can lower costs, serve more clients, and support small businesses. Although challenges like infrastructure and digital skills remain, technology offers vast opportunities for growth.

As African economies continue to develop, digital microfinance will play an essential role in promoting financial inclusion and empowering social enterprises. Understanding this impact helps stakeholders work towards stronger, more accessible financial systems for all.